Introduction

RITES Limited is an India Central Public Sector Enterprise primarily in the business of providing infrastructure consulting and engineering services, focussed towards the transport sector in India and abroad. The company’s business is closely aligned with the Indian Railways. It is the only export arm of Indian Railways for exporting rolling stock (other than Thailand, Malaysia and Indonesia). The company has 2 subsidiaries and 2 joint ventures operating in allied businesses

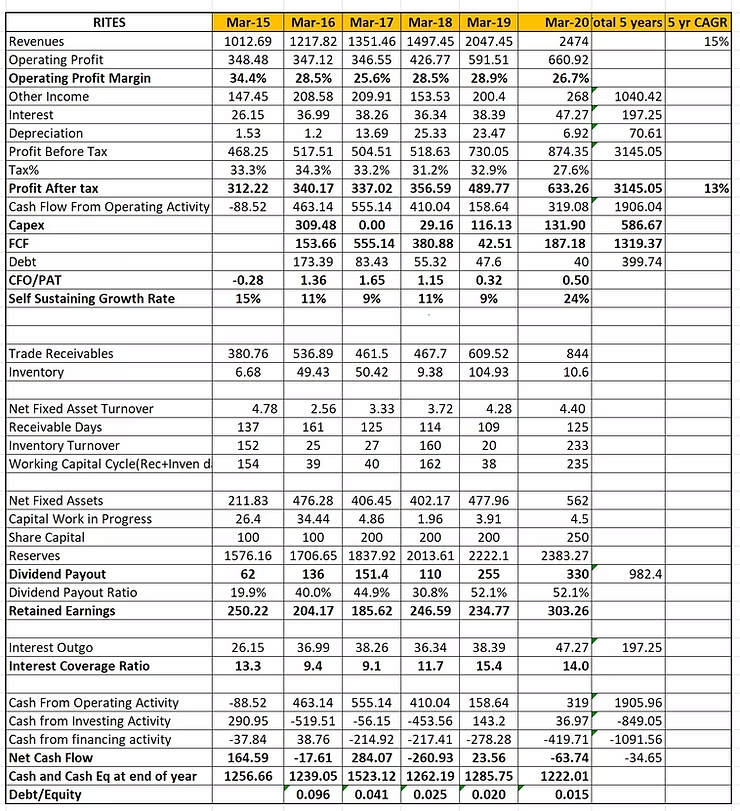

FY20 results were extremely good with the business having record consolidated revenues of 2734 crores, a PAT of 633 crores, both at a 6 year CAGR of 15% and 13% respectively. It can be said that 60-70% of the company’s revenues come from the railway sector and the remaining is a split between other areas such as roads and highways, urban transport, airports and seaports, inland waterways, etc.

The infrastructure sector in India is a major thrust area for the government of India having announced ambitious targets and massive stimulus. For instance, Indian government introduced ‘Bharatmala Pariyojana’ in 2017 a new highways program expected for completion in 2022 has planned total additions of 34,800 kms at an estimated cost of Rs.5.35 tn. Massive tendering activity is being undertaken in over 15 cities for metro rail construction. The railways too, has expanded its capex budget and is aggressively targeting line doubling, tripling of lines and electrification in the coming years.

RITES Business Areas:

- Consulting: is the company’s primary business. It a mainly cognitive pursuit with highly skilled engineers consulting engineering challenges. Some examples are evaluating feasibility of new road/rail corridors, creating detailed project reports, quality assurance services like third party inspection and vendor assurance services, complete project management consultancy, railway electrification, railway signalling and telecommunications to name a few. The company has completed very challenging works involving high technical complexity in civil engineering and operations management. About 60% of the consultancy income comes via the Indian railways and the rest from public and private companies in India and abroad.

- Leasing: involves mainly wet leases of rolling stock and DEMU sets to non-railway clients such as SAIL, L&T, Visakhapatnam Port Trust, Dhamra Port Trust, Paradip Port Trust, Tata steel, DVC, Bhilai steel Plant etc. Presently, 62 locomotives have been leased out.

- Exports: head consists largely (but not strictly) of developing, selling and maintenance of locomotives and coaches. Among the big orders the company has as are : Sri Lanka comprising of 10 diesel locomotives and 6 DMU train sets; recently won order of supply of 6 cape gauge Locomotives and 90 passenger coaches including DEMU train-sets to Mozambique worth Rs. 680 crore (there are 16 countries with rails on cape gauge and this new design opens up this niche market). The ability to design and develop locos for such unique markets comes with its linkage to the Indian Railways (Integrated Coach Factory) and a JV between RITES and SAIL called SAIL RITES Bengal Wagon Industry Pvt. Ltd.

- Turnkey Projects: involves construction work carried out for the Indian railways. Projects include doubling and tripling of railway lines, line electrification and signalling, setting up workshops for wagon refurbishment, designing & construction of Station Building (extension), FOBs, platform improvement, Lifts, Escalators, & face lifting of existing Station Building, etc. These projects are allocated either by internal bidding(mainly between IRCON , RVNL and RITES) or by direct nomination basis, as may be the case.

- Power Generation: is via a subsidiary called REMCL and is in the business of facilitating power procurement and producing power via renewable innovations like wind energy, solar roof coaches and panels along rail lines, etc. for the Indian railways.

Financial Performance:

Sources: Screener.in and company annual reports

- Overview: Sales has grown at a 5 year CAGR of 15% from 1217 cr to 2474 cr in FY 2020. During the same period, PAT has grown 13% from 340 cr to 633 cr. PAT margins have averaged 26% over this period.

- Free Cash flows and Capex: The company has generated a free cash flow of 1319 cr over the last 6 years. Conversion of net Profits to cash fluctuates quite a bit with the average ratio being about 0.8. This is because of high receivables the business faces. It can be seen that the business is very Capex light, which is unusual for a company operating in infrastructure. This is a massive plus point.

- Working Capital Cycle: 126 days. The management commentary on this is that many projects are quite large and time consuming. At present there is no liquidity challenge the company faces, this could become a challenge later on.

- Debt and Interest: The company has a very low debt to equity ratio of 0.015 and a favourable interest coverage ratio of 14.

- Dividends and Retained Earnings: The Company has paid about 40% of its cash flows from operations as dividends to shareholders over the last 5 years. The government being the majority stakeholder, the dividend policy is likely to be favouring investors seeking regular cash flows. The company is able to invest in retained earnings well to grow organically as is apparent in the healthy sales growth.

- Cash and Cash Equivalents (CCE): The company has a huge CCE reserve of upwards of 1200 crores. This surely puts the company in a very favourable position in uncertain times. This also presents a good opportunity to grow via M&A route.

- Other Key Ratios:

o Asset Turnover Ratio(Sales/Avg total Assets): Due to a low fixed asset base and revenues dependent on consulting, the company enjoys a healthy 4.4 ATR.

o Inventory Turnover: Due to an asset light model, this ratio is also very healthy presently standing at 233.

o Return on Equity: The average ROE over the last 5 years has been 19%

o Return on Capital Employed: The ROCE as on Mar2020 was 34% and has consistently been around the 30% mark for the last 5 years.

The financial performance of RITES paints a picture of a flexible company. It is a rare combination of high growth, strong cash position, high return on capital and low debt business. The company enjoys powerful parentage, and is leveraging its ability well to expand into export markets as well as private projects.

Business Performance:

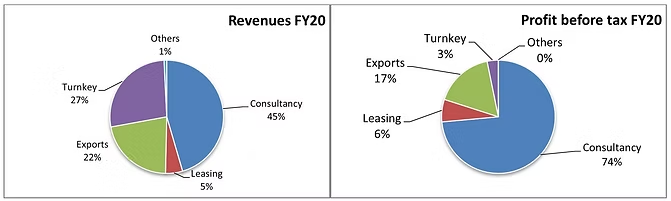

The consultancy business is the key competitive advantage that RITES enjoys, and it contributes to 3/4th of the total profits and just 45% in revenues. On the other end of the spectrum, Turnkey construction projects generate only 3% of the profits. The leasing and export business lie in between this trend.

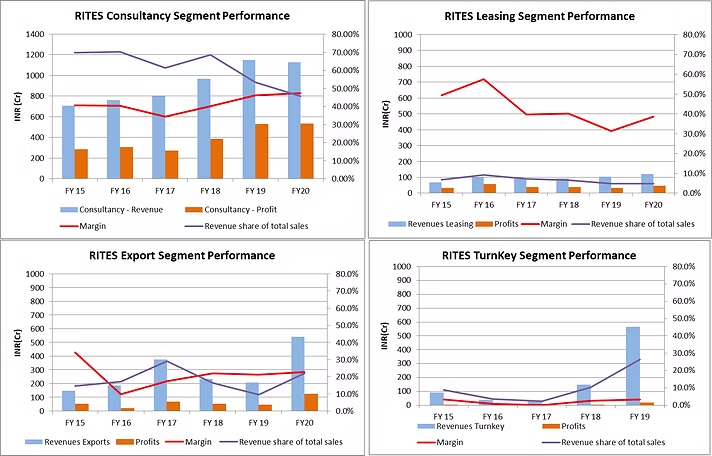

Segment Performance Analysis:

- Consultancy segment is growing at a 6 year CAGR of 8.1%. Profitability of this segment has grown at a rate of 10.9% and net profit margins are almost near 50%. This indicates improved operational efficiency. The share of revenues from consulting has fallen from 70% in 2015 to about 46% in 2020.

- Leasing Segment: Margins in the business are attractive at about a 40% average EBIT. 6 year CAGR sales growth is 10% and leasing revenues contribute only about 5% of the revenues. There is decent amount of predictability in this business due to the long term nature of lease contracts.

- Exports Segment: this is a high growth area for RITES, and in recent years, exports have grown at a CAGR of 24% with PAT margins in the mid 20’s. Recently the company has received large orders for exports and holds a healthy order book.

- Turnkey Segment: has grown at a rapid rate of 40% CAGR. However, is a low margin business. Has the effect of inflating overall sales numbers and putting pressures on profit numbers. According to the management, entering this business was important as many consultancy projects required turnkey solutions as well. The management maintains that the turnkey business will remain about 25-35% of revenues in the medium-long term.

- Power Generation and Station Development: are activities undertaken by RITES via its subsidiaries REMCL (49% holding) and IRSDC (recently 24% stake recently acquired for INR 48 crores). ISRDC is a SPV of the Indian railways with the main aim of (re)development of railway stations and improvement of passenger amenities at stations. While both these businesses contribute to less than 1% of business, they have potential for the future and investors will do well to see how these play out.

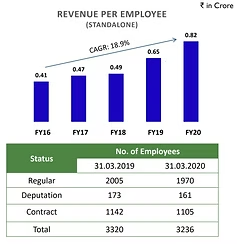

Theme of operational efficiency fuelled growth:

Source: Investor Presentation FY20

The number of employees over the last 6 years has remained almost stagnant (3200). However, employee costs as a percentage of total operational expenses in 2015 were 46%. In 2020, this number was 28%, a whopping 18 percent points decline over 6 years. The revenue per employee has grown at a CAGR of 18.9% over the same period! This reflects well on management.

During the same period, the company has grown in allied businesses such as exports and turnkey construction. RITES is now capable of providing end to end services in transport infrastructure segment making the company more competitive.

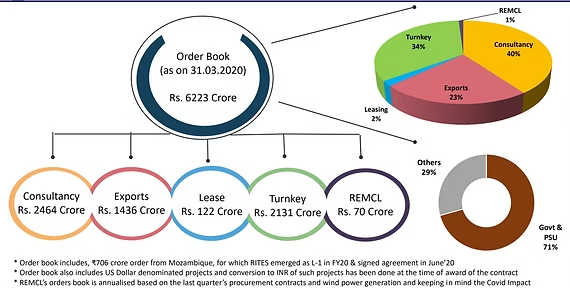

Order Book:

Source: Investor Presentation FY20

This translates to 2.5 years of current revenues. Management expects 8000 cr order book by end of 2020. Judging by past investor conference calls, management reliably forecasts future order book growth.

Covid Impact on Business

This section is based on the management discussion during Q4 F20 investor call and includes no personal views. The consultancy revenues ended flat in FY20 due to disruptions in the month of March. The lockdown impacted inspections on site and if business resumes in July, consultancy should be back to regular growth rates. There is also delay in award of some turnkey projects by the Indian railways owing which the order book is smaller than expected. Overall, barring some delays in execution, the company faces no material impact or loss in orders.

Shareholding and Management

RITES was listed on July 2, 2018 when the government of India divested 12.6% of its equity in the entity via an IPO on the National stock exchange. Thereafter, the government further diluted its stake to 72.02% leaving 27.98% with the public.

Mr. Rajeev Meherotra has been the Chairman and MD of the company for over 7 years and under his leadership, the company has improved operational efficiency and growth. The board is diverse with 5 whole time directors, 3 government nominee directors and 6 independent directors according to the FY 19 annual report. The board members do not own any significant shares within the company and their remuneration is well within prescribed limit of 5% of PAT. A study of annual reports of the last 5 years did not cause us to raise any red flags on the management. Experience during investor calls is very good, with management being transparent and answering a wide range of questions.

Risk Management

The company has a robust risk management policy in place. The company regularly manages currency rate risk by employing appropriate hedging instruments. As for credit risks, these are more influenced by the individual characteristics of each customer. Trade Receivables towards export sales are generally managed by establishing Letter of Credit with the clients. Further, most of the clients of the company are Government or Government Undertakings; hence credit risk is bare minimum. As many of the nation’s RITES does business with are under developed markets, this can turn up to be a cause for concern in the future and we have accounted for this in our valuation.

Valuation

Our DCF valuations for RITES assumed that the company will grow rapidly at a rate of 15% for 5 years post which we have assumed a terminal growth rate of 4%. The operating margin we have assumed during this high growth phase is 25%, and a cost of capital of 12%. Taking into account the cash and cash equivalents, we arrived at a fair value of 9730 crores, against a market capitalisation of 6039 crores.

Based on our DCF, we feel that the stock is available at a discount.

Other Key Discussion Areas:

- With sales being diluted by low margin turnkey business, the overall margins may be stressed. It will be important to keep an eye on the business split of the company, so that we can continue to value it as a primarily consultancy firm.

- RITES has acquired a 24% stake in Indian Railway Stations Development corporation for a sum of 48 crores. It’s other subsidiary REMCL has secured its largest mandate from Indian Railways for handling tendering, installation supervision and managing power supply from 3 GW solar power plants to be set-up on vacant Indian Railway Land. These are both exciting additions to the portfolio, but the economics of this is not totally clear. Being a government entity is a doubled edged sword, as there may be economically unviable projects that the company could be forced to undertake.

- Another change in dynamic is the mode by which the company wins new business. Earlier, majority of business was secured directly via government Nomination. The railway rules have been amended to incorporate closed bidding for projects. This might seem worrisome, but has benefits as well, as nomination was at a fixed profit margin, which will not be the case in bidding. The company is no alien to bidding as about 33% of it’s consulting business is via bidding and almost all the export business. The management has shown confidence in bidding and continuing to win projects.

- Provisions: The company has some pending payments which have been provisioned from export business arriving out of Africa. Management has suggested that the issue is ironed out, but this is something we see as a risk to the business.

- RITES is almost entirely equity funded and has a strong cash position. Having a strong credit rating, we would like to see the company raise some debt to lower the overall cost of capital.

Disclaimer: I am invested in RiITES Ltd. My views may be biased. Please do your due diligence before investing. If you have a contra-view, I would love to listen.